Do you know what kind of Life Insurance coverage you need for Final Expenses: Term Life or Whole Life?

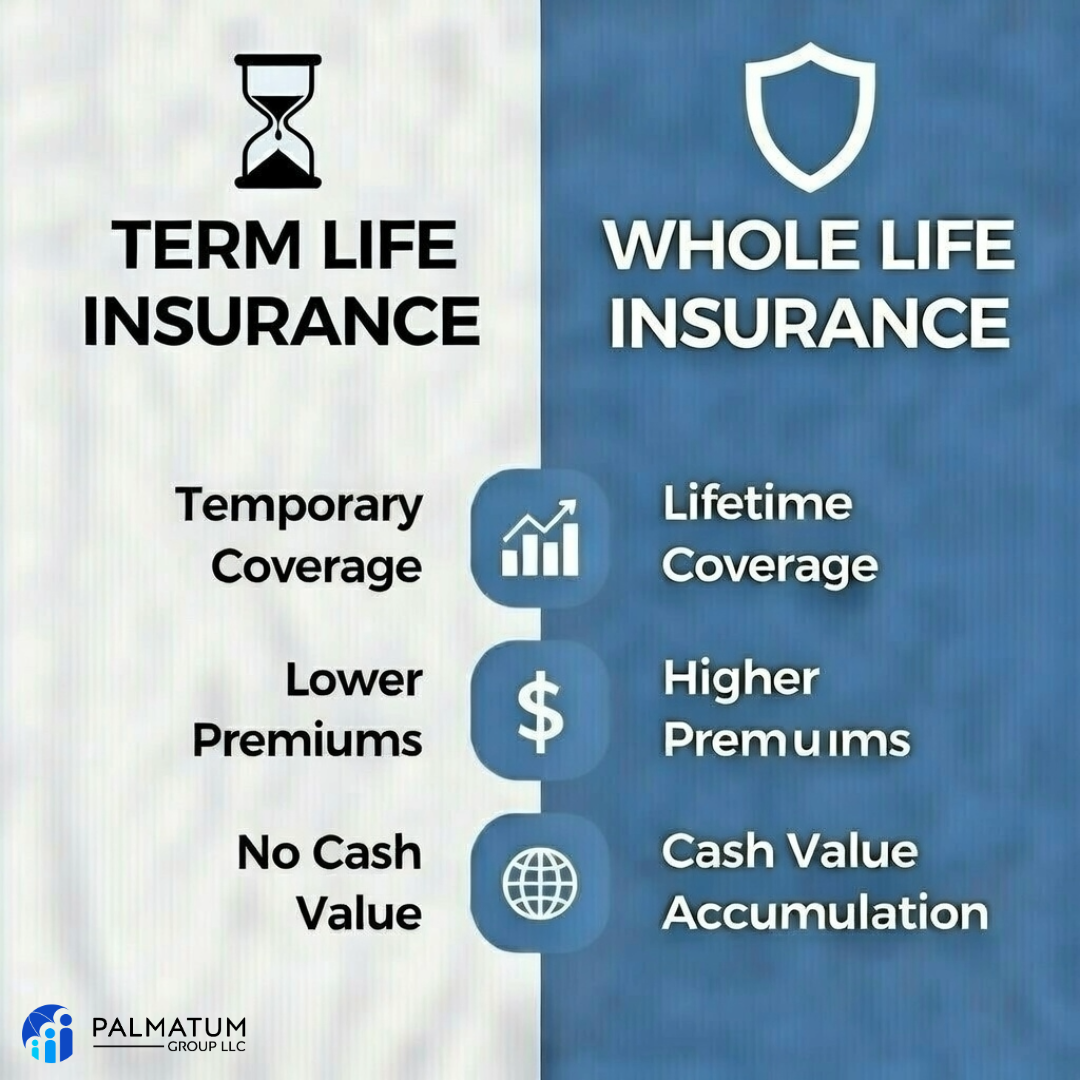

Term Life Insurance is basically "renting" insurance for a set period (examples: 10, 15, 20, or 30 years). You choose how long you need it (like until the kids are grown or the mortgage is paid off), pay relatively low premiums, and if you pass away during the term, your family gets a tax-free death benefit to help with lost income, debts, etc. If you outlive the term? Coverage ends with no payout—no refunds—but you had protection during the years you needed it most.

Cost: Term is generally cheaper because many policies expire without a claim, so insurers pay out on fewer of them.

Whole Life Insurance is designed to provide coverage for your entire lifetime (as long as premiums are paid). Premiums stay level for life, and the death benefit is guaranteed (assuming premiums continue). Plus, it builds cash value over time, which you may be able to borrow against or withdraw if needed (subject to policy terms).

Cost: Whole Life generally has higher premiums because coverage is designed to last your entire lifetime—the insurer expects to pay a death benefit eventually—and part of the premium funds the cash value feature.

For final expense planning (think funeral costs, burial, medical bills, or small debts—often averaging $10k+ these days), whole life (including smaller "final expense" whole life policies) is often a strong long-term choice, especially if you're older or want lifelong protection.

Here's why many people choose Whole Life Insurance for Final Expense Coverage:

Term might expire before you pass away (most people live past 70–80+), leaving no coverage when those final costs arise.

Whole life stays in force your whole life (as long as premiums are paid), so it can help your loved ones cover expenses without draining savings or going into debt.

Many of these policies require no medical exam—just health questions to qualify.

The built-in cash value can sometimes provide funds later in life if needed.

It eliminates the risk of outliving term coverage and leaving family to pay out-of-pocket.

That said, term can be a great, affordable fit for temporary needs like income replacement. Everyone's situation is different!

What are you thinking about—covering yourself, a parent, or planning ahead?

Reach out via email for a no-obligation phone consultation to explore your options: jon@palmatumgroup.com